HIGHLIGHTS

OVERVIEW

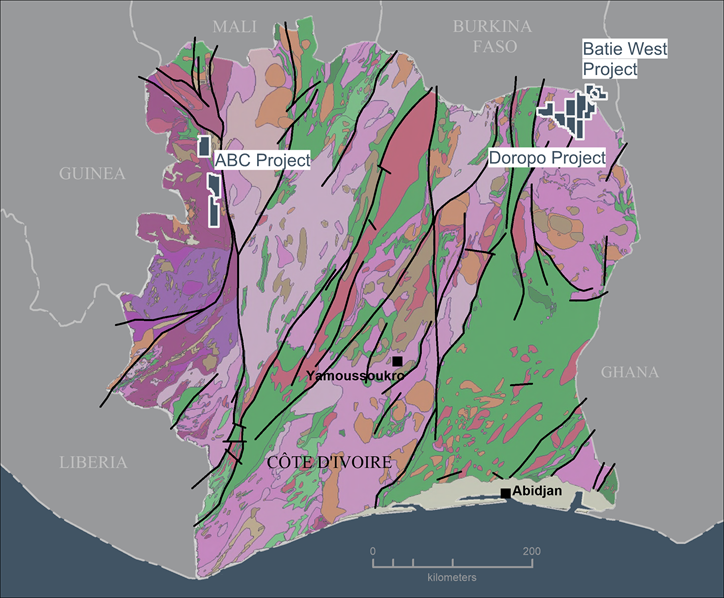

The Doropo Project (“Doropo”) consists of seven exploration permits, covering an area of approximately 1,850km2. Doropo is in the northeast of Côte d’Ivoire, approximately 480km north of Abidjan.

The Doropo Project (“Doropo”) consists of seven exploration permits, covering an area of approximately 1,850km2. Doropo is in the northeast of Côte d’Ivoire, approximately 480km north of Abidjan.

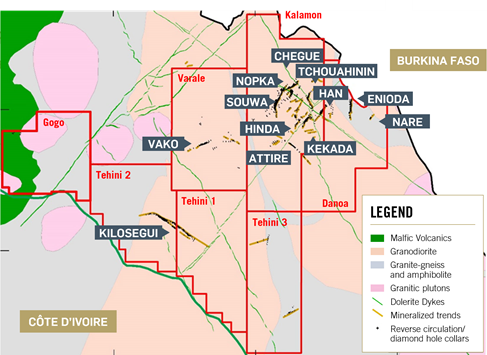

The license holding covers thirteen gold deposits, named Souwa, Nokpa, Chegue Main, Chegue South, Tchouahinin, Kekeda, Han, Enioda, Hinda, Nare, Kilosegui, Attire and Vako. Approximately 85% of the gold deposits are concentrated within a 7km radius (“Main Resource Cluster”), with Vako and Kilosegui deposits located within an approximate 15km and 30km radius, respectively.

Geologically, Doropo lies entirely within the Tonalite-Trondhjemite-Granodiorite domain, bounded on the eastern side by the Boromo-Batie greenstone belt, in Burkina Faso, and by the Tehini-Hounde greenstone belt on the west.

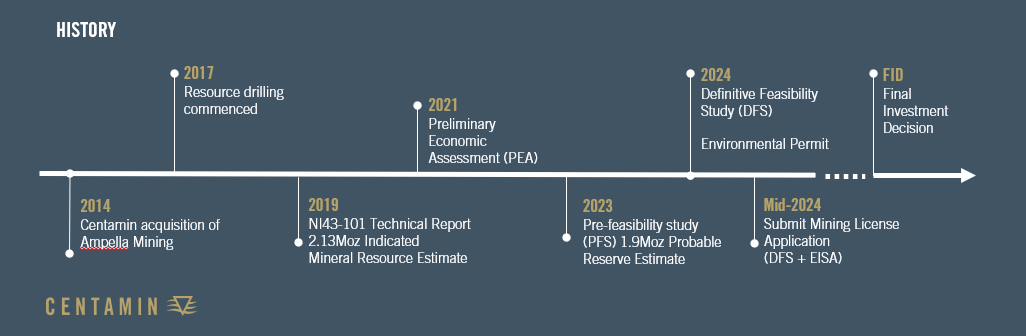

The Company began extensive exploration at Doropo in 2016, building to a Mineral Resource Estimate of 5Moz in 2021. As part of the PFS work programme, a maiden Mineral Reserve of 1.87Moz was declared in the Probable Reserves category. The project is being progressed through to the DFS stage which is scheduled for completion in mid-2024.

2023 Doropo NI43-101 Technical Report

The Doropo landholding lies entirely within the granitic domain, bounded on the eastern side by the Boromo-Batie greenstones belt, in Burkina Faso, and on the western side by the Tehini-Hounde greenstones belt.

At the Project scale, the geology consists of fairly homogeneous medium to coarse grained granodiorite. Several of the deposits are intersected by regional, post-mineralisation diorite dykes.

Gold mineralisation occurs associated with discrete structurally controlled zones of intense silica- sericite alteration, focused within and along the margins of narrow (5-10 m wide to locally 20-25 m) shear zones. Outside of the mineralised zones, the granodiorite is fairly undeformed. The mineralised zones generally form clearly identifiable tabular bodies although this is complicated where two structures intersect, such as at the Nokpa deposit.

Gold grades within the mineralised zones are generally very variable and exhibit positively skewed grade distributions with relatively high Coefficients of Variation.

The currently defined mineral resource is formed of 13 deposits that lie within a 25km radius. 11 of these deposits are within a 7km radius, with Vako and Kilosegui 15km and 30km to the Southwest of the Main Cluster.

The results of the 2023 PFS meet the Company's internal hurdle rates. The DFS and ESIA work programmes are underway and scheduled for completion in mid-2024. Completed in 2023 confirms the economic viability of the project and suggests that it has the scale and potential to be Centamin’s next mine development:

-

2.5Moz of Indicated Resources, inc.1.9Moz of Probable Reserves @ 1.44g/t Au

-

Annual gold production of 173koz over the LOM, with an average of 210koz in the first five years

-

All-in sustaining costs of US$1,017/oz over the LOM, with an average AISC of US$963/oz for the first five years

-

Construction capex of US$349 million, inclusive of a 10% contingency

-

Project PFS meets internal investment criteria at long term economic assumptions (gold and diesel price)

-

US$497M post-tax net present value ("NPV8%") with a 41% IRR at US$1,900/oz gold price

- US$330M post-tax NPV5% with a 26% IRR at US$ 1,600/oz gold price

PROJECT OVERVIEW

Mining & geology

- 8 pits, shallow dipping structures with consistent geology

- Truck and Shovel, Multiple shallow pits

- 4.1x, LOM Strip Ratio (waste to ore)

Processing

- SAG/Ball mill and CIL, Conventional flowsheet

- Avg. 4.4Mtpa Throughput, 4.0Mtpa (fresh ore)

5.4Mtpa (oxide/transition ore) - 75/106 Micron Grind Size, Non-Refractory

- 92% Gold recovery over the LOM

Infrastructure

- Tailings storage facility

- Full geomembrane lined, downstream construction

ANCOLD, GISTM Guidelines - 90kV national Ivorian grid

- 55km connection from Bouna sub station

DEFINITIVE FEASIBILITY STUDY

There remains further upside opportunities which will be assessed during the DFS, including:

- Mineral Resource upgrades

- Resource extensions along strike

- Regional exploration of target areas

- Operational cost-saving optimisation

- Construction cost-saving opportunities

MINERAL RESOURCES

Inclusive of Mineral reserves. Please refer to the Group Reserve and Resources page for all notes.

Cut-off grades: 0.3g/t

| October 2023 | |||

| Category | Tonnage (Mt) | Grade (g/t) | Gold Content (Moz) |

| Measured | 1.5 | 1.6 | 0.1 |

| Indicated | 75.3 | 1.25 | 3.0 |

| Measured +Indicated | 76.9 | 1.26 | 3.1 |

| Inferred | 7.4 | 1.23 | 0.3 |

MINERAL RESERVES

Varied cut-offs 0.39g/t to 0.71g/t

| June 2023 | |||

| Category | Tonnage (Mt) | Grade (g/t) | Gold Content (Moz) |

| Proven | - | - | - |

| Probable | 40.6 | 1.44 | 1.9 |

| P & P | 40.6 | 1.44 | 1.9 |